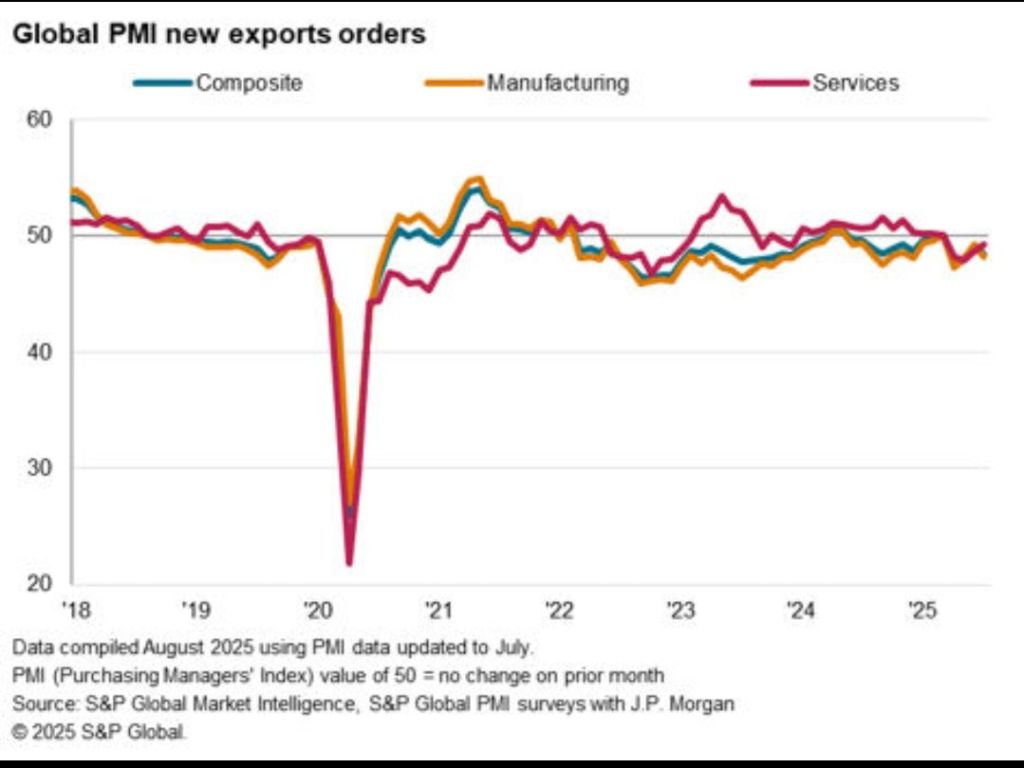

The global manufacturing ecosystem has always moved in cycles, but what we are witnessing today is not just a routine slowdown—it is a structural recalibration. Historically, manufacturing demand has been closely tied to global consumption patterns, trade openness, and industrial confidence. From the post-2008 recovery phase to the pandemic-induced disruptions and subsequent rebound, manufacturing has oscillated between resilience and fragility. However, the current slowdown, particularly in Europe, reflects deeper issues—energy transitions, geopolitical fragmentation, and demand fatigue—rather than a temporary dip.

Europe’s Demand Contraction and Its Ripple Effects

Europe has traditionally been a major demand center for global manufacturing exports, especially for countries like India, China, and Southeast Asian economies. Today, however, high energy costs, tight monetary policies, and subdued consumer sentiment are compressing industrial demand. Germany, often referred to as the manufacturing engine of Europe, has shown signs of stagnation, with reduced industrial output and weak new orders. This contraction is not isolated—it is cascading through global supply chains. Export-driven economies are facing shrinking order books, delayed shipments, and increasing price pressures, forcing firms to rethink their dependence on a few large markets.

Export-Led Growth Under Stress

For decades, export-led growth has been a cornerstone strategy for emerging economies. The assumption was simple: produce efficiently, integrate into global value chains, and tap into advanced economies’ consumption. But the current slowdown exposes a critical vulnerability—overdependence on external demand. Countries that built their industrial strategies around Europe and the US markets are now facing a demand vacuum. Indian sectors such as textiles, engineering goods, and auto components are already experiencing slower export growth, reflecting how tightly domestic manufacturing is linked to global cycles.

From Cyclical Slowdown to Structural Shift

What makes this slowdown particularly significant is that it may not be purely cyclical. Europe is undergoing a structural transformation driven by decarbonization policies, digital transition, and reshoring tendencies. The Carbon Border Adjustment Mechanism (CBAM), for instance, is not just a climate policy—it is reshaping trade flows and manufacturing competitiveness. Simultaneously, firms in developed economies are reconsidering long global supply chains in favor of regionalization. This means that even when demand recovers, the pattern of trade may not revert to its previous form.

Implications for Indian Manufacturing: Between Risk and Opportunity

For India, the slowdown presents a dual challenge. On one hand, reduced export orders can impact capacity utilization, employment, and MSME viability. On the other hand, it opens a strategic window to reposition itself. The China+1 strategy, ongoing supply chain diversification, and geopolitical realignments provide India an opportunity to capture market share—provided it addresses its internal constraints. Issues such as logistics costs, compliance burden, quality consistency, and technology adoption remain critical bottlenecks. Without resolving these, India risks being a marginal beneficiary rather than a major player in the evolving global order.

The MSME Vulnerability Trap

The slowdown disproportionately affects MSMEs, which are often the backbone of export supply chains but lack the resilience of large firms. Reduced orders translate directly into cash flow stress, delayed payments, and even closures. Unlike large corporations, MSMEs have limited access to credit, weaker bargaining power, and minimal risk-hedging mechanisms. This creates a vulnerability trap where global demand shocks quickly translate into local economic distress. The policy response, therefore, cannot be generic—it must be targeted, timely, and aligned with ground realities.

Rethinking Industrial Strategy: Beyond Export Dependence

The current phase demands a fundamental rethink of industrial strategy. Relying solely on export markets is no longer sustainable in a world characterized by uncertainty and fragmentation. Countries need to balance export orientation with strong domestic demand creation. India’s large internal market offers a unique advantage, but it requires income growth, consumption expansion, and infrastructure development to fully realize this potential. At the same time, diversification of export destinations—towards Africa, Latin America, and emerging Asia—can reduce dependence on traditional markets like Europe.

The Future: Resilient, Regional, and Technology-Driven Manufacturing

Looking ahead, manufacturing will increasingly be shaped by three forces: resilience, regionalization, and technology. Supply chains will prioritize reliability over cost efficiency, leading to shorter and more diversified networks. Digital technologies—AI, automation, and data analytics—will redefine productivity and competitiveness. Sustainability will become a non-negotiable factor, influencing both production processes and market access. In this new paradigm, countries that can integrate these elements into their industrial ecosystems will emerge stronger.

A Wake-Up Call, Not a Crisis

The slowdown in global manufacturing demand, particularly in Europe, should not be seen merely as a crisis but as a wake-up call. It highlights the limitations of existing growth models and underscores the need for strategic recalibration. For India, the path forward lies in building a more resilient, diversified, and innovation-driven manufacturing base—one that is not overly dependent on external demand but capable of shaping its own growth trajectory in an increasingly uncertain world.

#GlobalManufacturing #ExportSlowdown #EuropeDemand #IndustrialStrategy #MSMEs #SupplyChains #CBAM #ChinaPlusOne #Decarbonization #ResilientEconomy

Leave a comment