The global shift toward electrification—anchored in electric vehicles (EVs) and battery storage systems—marks one of the most significant structural transformations since the industrial revolution. What began as a climate-driven narrative has now evolved into a geopolitical and industrial race. Yet, beneath the optimism of rising investments lies a more complex reality: the cost economics of the EV and battery ecosystem are still in transition, shaped by technological uncertainty, supply chain vulnerabilities, and evolving market structures.

From Fossil Dependence to Electrification Ambitions: A Historical Realignment

Historically, energy systems were built around centralized fossil fuel infrastructures, with oil defining mobility and coal anchoring power generation. The EV revolution challenges this paradigm by shifting dependence from oil wells to mineral reserves—lithium, cobalt, nickel, and rare earths. This transition mirrors earlier industrial shifts, where control over critical inputs determined economic power. Today, instead of OPEC, the focus has moved toward mineral-rich geographies and processing capabilities, particularly in regions like Latin America, Africa, and China. However, unlike fossil fuels, the battery ecosystem requires a more complex value chain—from mining to refining, cell manufacturing, pack assembly, and recycling—making cost optimization a far more intricate process.

Investment Surge vs Economic Reality: The Cost Curve Still in Motion

Over the past decade, global investments in EVs and battery storage have surged, driven by policy incentives, climate commitments, and corporate strategies. Battery costs have fallen significantly—from over $1,000 per kWh a decade ago to near $130–150 per kWh in recent years—yet the pace of decline has slowed. Input cost volatility, especially lithium price spikes seen in 2022–23, exposed the fragility of the cost structure. While prices have moderated, the underlying issue remains: the industry has not yet achieved a stable cost floor.

Moreover, EV affordability continues to hinge on subsidies in many markets. Without incentives, EVs often remain costlier upfront than internal combustion engine (ICE) vehicles, particularly in price-sensitive markets like India. Total cost of ownership (TCO) may be favorable over time, but consumer behavior is still driven by initial purchase price, infrastructure availability, and perceived reliability.

Grid Storage and Renewable Integration: The Silent Backbone with Its Own Challenges

Battery storage is increasingly becoming the backbone of renewable energy integration, addressing intermittency issues in solar and wind power. However, the economics of grid-scale storage remain equally fluid. The levelized cost of storage (LCOS) varies significantly depending on technology, duration, and geography. While short-duration storage is approaching viability, long-duration storage solutions—critical for deep decarbonization—are still expensive and technologically evolving.

This creates a paradox: renewable energy is becoming cheaper, but integrating it reliably into the grid requires investments in storage that are not yet economically optimized. As a result, energy systems are entering a hybrid phase where fossil fuels still provide backup, delaying the full realization of a clean energy transition.

Supply Chain Geopolitics: The New Oil Wars of the Battery Age

The EV and battery ecosystem has introduced a new layer of geopolitical competition. China’s dominance in battery manufacturing and mineral processing has created strategic dependencies for Western economies. Efforts to diversify supply chains—through policies like the U.S. Inflation Reduction Act or Europe’s Critical Raw Materials Act—are reshaping global trade patterns.

India, too, is positioning itself through production-linked incentives (PLI) and localization strategies. However, the challenge is not just manufacturing cells but securing upstream resources and developing downstream ecosystems, including recycling. Without this integration, cost competitiveness will remain elusive.

Technology Uncertainty: Betting on a Moving Target

Another critical dimension is technological uncertainty. While lithium-ion batteries dominate today, alternatives such as solid-state batteries, sodium-ion technologies, and hydrogen-based systems are gaining attention. Each promises improvements in cost, safety, or energy density, but none has yet achieved commercial scalability.

This creates a strategic dilemma for investors and policymakers: commit heavily to existing technologies or hedge bets across multiple innovations. The risk of technological obsolescence adds another layer of complexity to cost economics, as investments may not yield expected returns if the technology landscape shifts rapidly.

India’s Opportunity and Constraint: Scale without Cost Leadership Yet

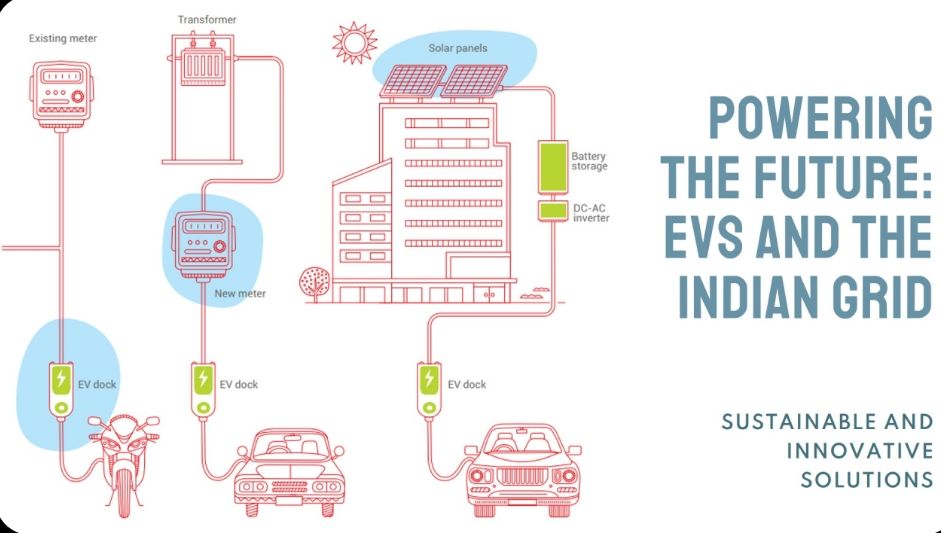

India stands at a unique juncture. With one of the largest potential EV markets and ambitious renewable energy targets, the country has the scale to drive demand. However, cost sensitivity remains a defining constraint. Two-wheelers and three-wheelers are leading EV adoption, reflecting a pragmatic shift toward segments where cost economics are more favorable.

Yet, for four-wheelers and commercial vehicles, the transition is slower. Charging infrastructure gaps, financing challenges, and high battery costs continue to limit adoption. On the grid side, India’s push toward renewable energy is creating demand for storage, but large-scale deployment is still in early stages due to cost considerations.

The Next Decade: From Subsidy-Driven Growth to Market-Led Sustainability

The future of the EV and battery ecosystem will depend on a critical transition—from policy-driven expansion to market-driven sustainability. This will require breakthroughs in three areas: cost reduction through scale and innovation, supply chain diversification to reduce volatility, and business model innovation to enhance affordability (such as battery leasing and swapping).

Recycling and circular economy models will also play a crucial role in stabilizing costs by reducing dependence on virgin raw materials. As the first generation of EV batteries reaches end-of-life, the recycling industry could become a key pillar of the ecosystem.

Transition Without Illusion

The narrative of the EV and battery revolution is often framed as inevitable and rapid. However, the reality is more nuanced. The transition is underway, investments are rising, and technological progress is evident—but the economics are still evolving. This is not a linear transformation but a phased adjustment, where cost, technology, and policy will continue to interact dynamically.

The real question is not whether the transition will happen, but how efficiently and equitably it will unfold. Those economies that can align technology, supply chains, and cost structures will emerge as leaders in this new energy order. For others, the risk is not just missing the transition, but being locked into a system where the promise of electrification remains economically out of reach.

#EVTransition #BatteryEconomics #EnergyStorage #ElectricMobility #CleanEnergyShift #SupplyChainGeopolitics #LithiumEconomy #IndiaEnergyFuture #Decarbonization #FutureOfMobility

Leave a comment