For nearly three decades, global textile and apparel trade has run on cost efficiency, scale, and speed — a system fuelled by fast fashion, outsourced production, and complex, opaque supply chains stretching across Asia. But that model is now approaching a decisive turning point. The European Union’s upcoming textile sustainability and circularity rules — centred on recycled content mandates, full traceability requirements, and emissions accountability — are set to transform apparel sourcing strategies worldwide between 2026 and 2027.

This is not merely regulatory tightening; it is the beginning of a structural shift in how fashion is produced, traded, monitored, and consumed.

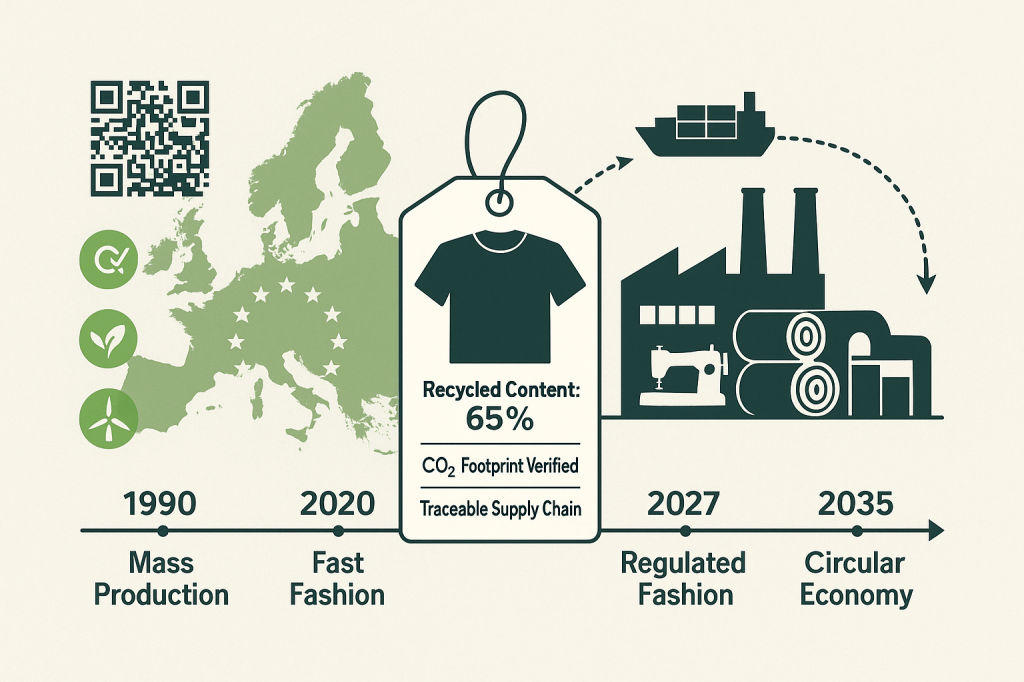

From Mass Production to Accountability

The global textile industry has evolved through three defining eras:

Era Driver Outcome

1970s–1990s Cost-shifting + globalisation Offshoring of manufacturing from EU/US to Asia

2000s–2020 Fast fashion + e-commerce scale Mass consumption, high waste, low transparency

2023 onward Climate regulation + circular economy Compliance-led growth, digital traceability, recycling mandates

Europe’s new textile rules align with its broader Green Deal mandate, positioning sustainability as not a voluntary branding choice, but a legal compliance requirement tied to market access. Unlike earlier corporate-led sustainability commitments, these regulations carry enforceable penalties, digital tracking obligations, and carbon-linked reporting frameworks.

What the New EU Rules Demand

Between 2026 and 2027, textile exporters will need to comply with:

Mandatory Recycled Fibre Content (for categories like polyester and cotton)

Digital Product Passports with QR-based traceability from farm to finished garment

Restrictions on ultra-fast-fashion business models

Lifecycle emissions reporting (Scope 1, 2, and critical Scope 3)

Design-for-durability and repair obligations

Extended Producer Responsibility (EPR) fees on waste

This means the EU will stop accepting cheaply produced garments with unclear origins, questionable labour records, and minimal environmental accountability — the exact supply chain model that enabled “fast and disposable” fashion for the past 15 years.

A Cost Shock or a Competitive Reset?

For exporters, especially in India, Bangladesh, Turkey, Vietnam, and China, compliance will increase costs in the short term due to:

Investment in recycling technologies

Better-quality fibres and dyes

Digital traceability platforms

Renewable-energy integration

Labour and ESG certification upgrades

However, the global market is also shifting. Major European retailers are signalling willingness to pay a compliance premium — not for branding optics, but to avoid penalties and border rejections.

Factories with circular production capacity, wastewater certification, and renewable-powered operations could become preferred long-term sourcing partners.

Winners vs. Vulnerable Players

Likely Winners 2026 and beyond

✔ Suppliers with audited transparency

✔ Mills with mechanical/chemical recycling capacity

✔ Regions investing in renewable energy and ESG compliance

✔ Fibre innovators (bio-based textiles, traceable cotton, recycled polyester)

At Risk:

Ultra-low-cost suppliers

Informal and fragmented supply chains

Small units unable to digitalize traceability

Exporters dependent on virgin synthetic fibres

Fast fashion giants may shrink, consolidate, or pivot to rent-repair-reuse ecosystems — a business model already scaling in Europe.

A New Geography of Apparel Sourcing

As environmental compliance becomes a prerequisite for market entry, sourcing could shift from volume-led hubs to capability-led ecosystems.

India, for instance, could gain ground if it aligns policy with:

National textile traceability system

Domestic recycling infrastructure

Carbon-neutral spinning and dyeing zones

FTAs aligned with EU sustainability benchmarks

Countries unable to modernize may lose access despite cost advantages.

The Textile Passport Economy

By 2030, every garment entering Europe may carry:

Its material composition

Emissions history

Labour compliance footprint

Repairability score

Reuse and recycling pathway

Fashion could shift from ownership to circular usage models, with new business opportunities emerging in digital certification, reverse logistics, textile recycling, and second-life manufacturing.

The textile industry, once a symbol of disposable consumption, could become a digital, data-verified circular economy ecosystem.

Regulation as a Catalyst for Reinvention

The EU’s 2026–27 textile strategy is not merely regulation — it is a system redesign.

It will reshape:

What materials are grown,

How factories are powered,

How garments are designed,

And how consumers value clothing.

The industry now stands at the inflection point last seen when globalisation shifted production offshore in the 1990s.

This time, the shift isn’t about cost efficiency — it is about carbon efficiency, traceability, and circularity.

For those who adapt, the opportunity is historic.

For those who don’t, the market gate will quietly — but firmly — close.

Leave a comment